Do You Know Your Credit Score and Why It Matters

Using money today looks very different than it did in the “old days.” With apps like Venmo, Cash App, and Chime, fewer people rely on checks, and even cash is becoming less common. But regardless of how you pay for everyday purchases, when it comes to larger expenses, credit still plays a major role.

Credit is the ability to purchase goods and services without paying upfront, based on the understanding that you’ll repay the money later.

When a lender considers giving you money, they’re evaluating how likely you are to pay it back. The interest you pay is essentially the cost of borrowing—it’s how the lender makes money for letting you use their funds over time. If a lender sees you as a higher risk, they may charge a higher interest rate to offset that risk. That’s why keeping your rate low can save you a significant amount of money in the long run.

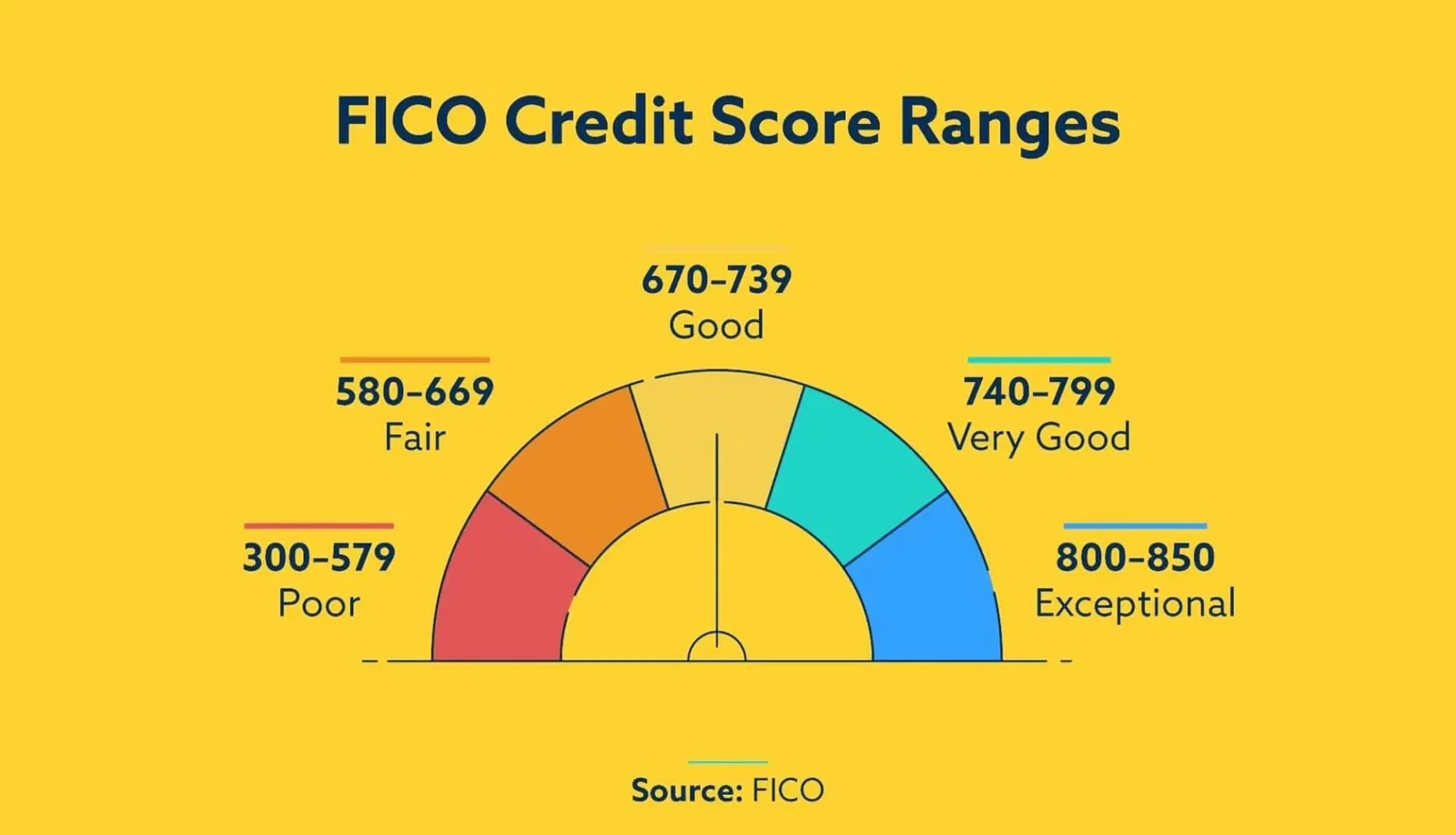

Your credit score is what lenders use to gauge your reliability. It’s often referred to as a FICO score, named after the company Fair Isaac that developed the original model widely used by lenders. Today, there are three major credit bureaus that track and report your credit activity: Experian, Equifax, and TransUnion.

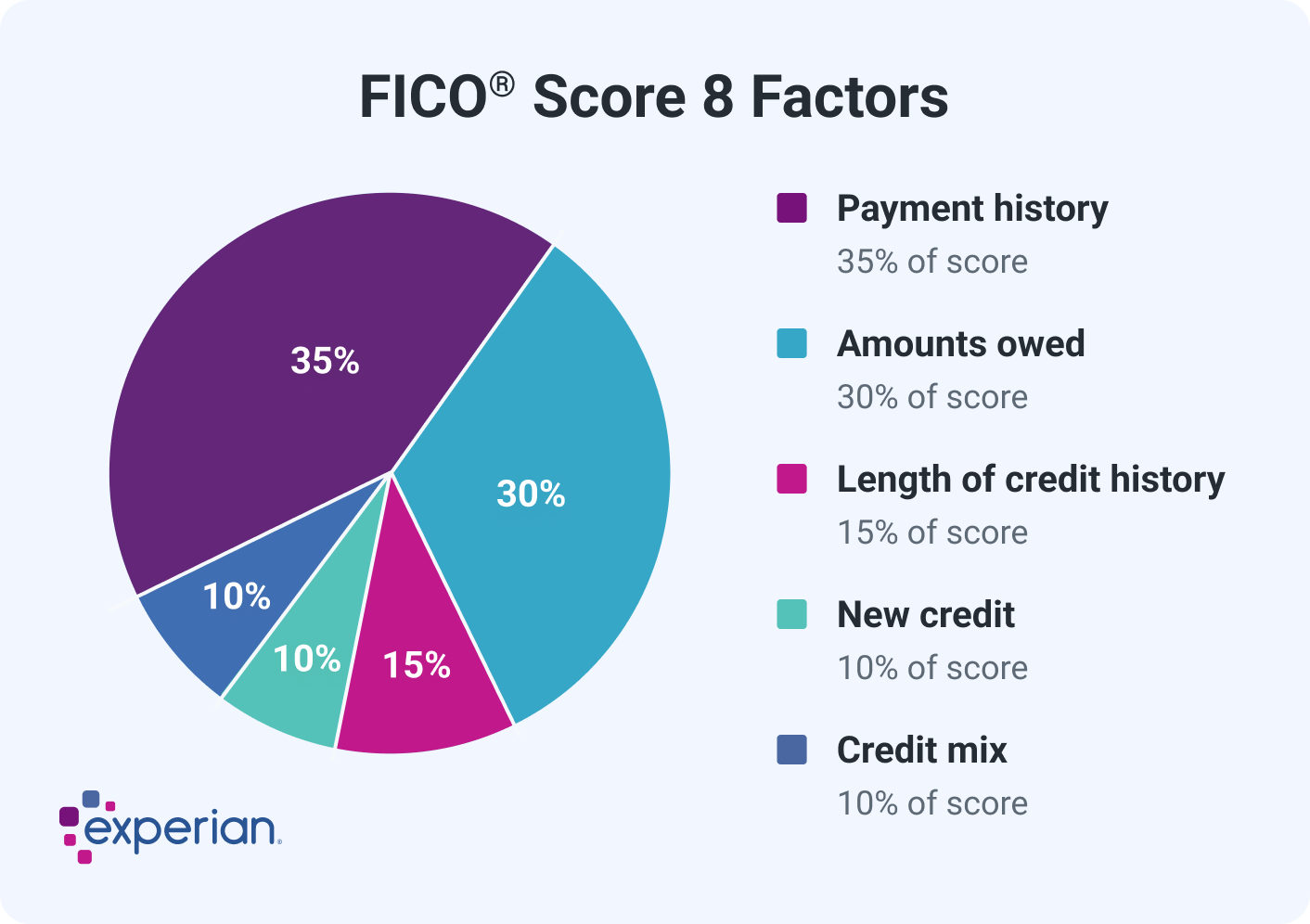

While each bureau may calculate your score slightly differently, they generally consider the same key factors:

Payment history (35%)

Amount of debt (30%)

Length of credit history (15%)

Credit mix (10%)

Recent credit inquiries (10%)

These factors may seem straightforward, but in practice, they can sometimes work against you. For example, it’s important to have credit, but not too much—since high debt can hurt your score. You want to avoid late payments, but even paying off a balance can sometimes cause a temporary dip. Applying for new credit can also lower your score. Because of this, it’s normal for your score to fluctuate—sometimes by as much as 30 points in a single month.

If you’re working toward a specific goal, like reaching a 640 score to qualify for a Virginia Housing mortgage, timing matters. You’ll want to avoid opening new credit cards, making large purchases, or even paying off significant balances right before your score is pulled.

If your credit isn’t where you’d like it to be, free financial counseling is available. Counselors can meet with you in person or over the phone to review your situation and help you build a plan to improve your score. Working with a counselor can also help you access certain mortgage assistance programs.

Many of these programs are designed for “qualifying” households, meaning your gross income (before taxes) must be at or below 80% of the Area Median Income (AMI). The Charlottesville area chart (which includes Nelson County) can help you see where you fall.

In general, improving your credit score comes down to reducing your debt—ideally keeping your credit utilization below about 25-35% of your available credit—making payments on time, and avoiding unnecessary credit inquiries.

Know what your credit score is? Go find out! There are many ways to do this. You can check directly with the Credit Bureau Websites/Apps, AnnualCreditReport.com, many Banking & Credit Card Apps offer credit scores for free as well as third party services like Credit Karma.