So You Want to Buy a House? Let’s Find Out How Much You Can Afford.

Welcome to our first post in our Homebuyer Blog Series! We here at NCCDF spend a lot of time running the numbers on affordability and explaining what affordability is. Frankly, it’s very dependent on the financial details of each individual family.

From an industry standpoint, affordability starts with income.

In housing and mortgage lending, the widely accepted benchmark is that your total housing costs should not exceed 30–33% of your gross monthly income. This standard is used by lenders, financial planners, and organizations like the U.S. Department of Housing and Urban Development.

What Counts Toward That 30–33%?

Whether you're renting or buying, the calculation includes:

Rent or mortgage payment

Property taxes

Homeowners insurance

Homeowners Association dues (if applicable)

Utilities (in many affordability models)

When buying, lenders often call this the “front-end ratio” — the percentage of your gross income that goes toward housing expenses.

Sometimes, however, the conversation starts with a home price - let’s say you spend a little time on Zillow or Realtor.com - and you see a house that piques your interest! It’s a “starter” home and it’s 3 bedrooms, 1.5 bathrooms on 3 acres in Arrington. It’s so cute and you can see yourself living there. The price is $215,000. How do you figure out if you can afford it?

There are plenty of mortgage calculators out there—you can get a quick estimate in just a couple of seconds. But it’s still helpful to understand the factors that go into the numbers. Here’s a link to one calculator that’s especially useful.

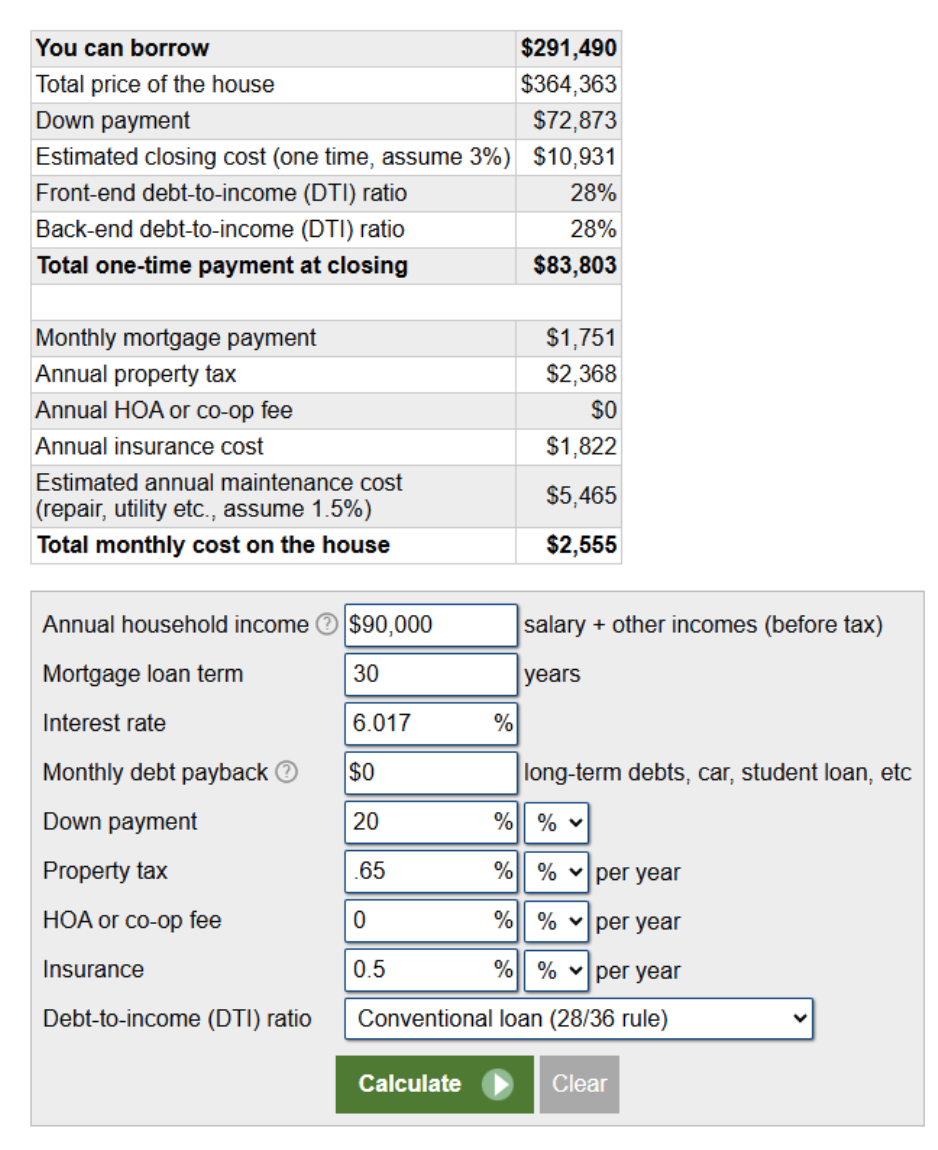

Start by entering your gross annual income (before taxes) from all sources. For example, let’s say you and your spouse both work and together earn $90,000 per year. Choose a traditional 30-year mortgage and assume an interest rate somewhere around 6%.

You can also add other debts into the calculator—things like car payments or student loans—so it reflects your full financial picture. Don’t forget to include your down payment, too. Have you set aside money for one yet? (We’ll cover that topic in a future blog post!) For now, let’s assume you’ve saved 20%.

Next, add property taxes. In Nelson County, the rate is 0.65%—that’s 65 cents for every $100 of property value. You’ll also want to estimate about 0.5% for homeowners insurance.

Finally, most conventional loans look closely at your DTI (debt-to-income) ratio—the percentage that compares what you owe to what you earn. Lenders use this number to determine how much they’re willing to lend you.

Using a calculator with these factors included can give you a good first estimate. It will show both the loan amount you might qualify for and the total home price you may be able to afford. It can also provide a realistic picture of how much you’ll need to save for a down payment and what your monthly costs might look like.

Those monthly costs typically include P&I (principal and interest on the loan) along with property taxes and homeowners insurance. Taxes and insurance are often included in your monthly mortgage payment and held in an escrow account by your lender, who then pays those bills when they come due.

Here’s what our calculator came up with:

There you have it—you could afford a $215,000 home. But wow… that down payment! Do you happen to have a rich uncle hiding somewhere?

All jokes aside, the down payment can feel like a big hurdle. Luckily, if you’re selling a previous home, you might be able to roll some of that equity into your new down payment to lower your mortgage. And hey, if you do have a generous uncle, even better!

The last thing to consider is your monthly payment. This is often the best way to gauge whether a home is truly affordable for you.

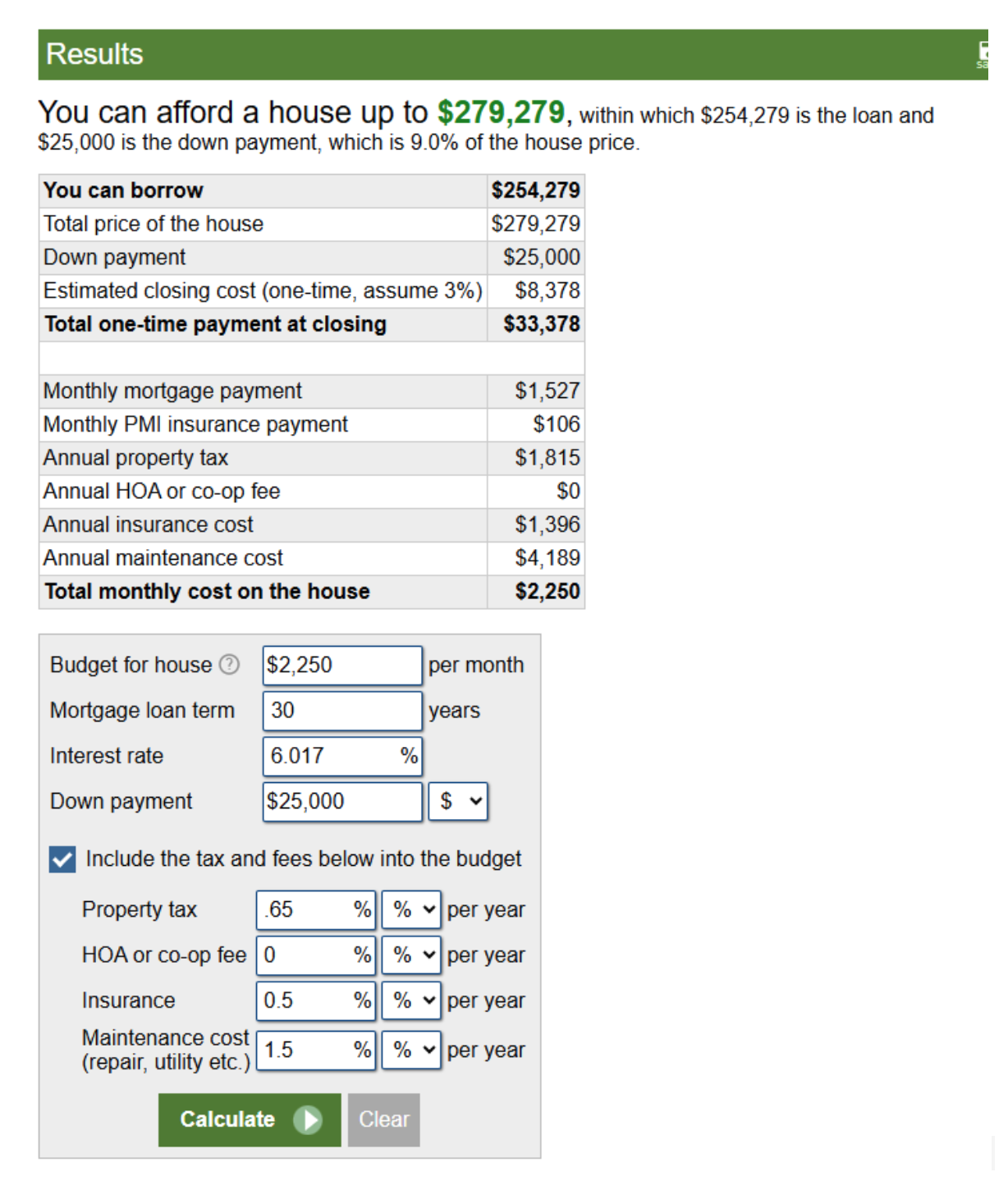

Here’s a simple way to estimate it: take your annual salary, divide it by 12 to get your monthly income, and then multiply that by 30% (or 0.3). That gives you a rough idea of what you could comfortably spend on housing each month.

$90,000 ÷ 12 = $7,500 X .3 = $2,250

This calculation shows you what 30% of your gross income is monthly and then you can look at the monthly mortgage payment above which includes taxes, insurance and maintenance (which is very important too and we’ll do another blog post just on that!) and see that it’s very close to your 30% affordability. Now, this particular calculus does NOT include utilities and it does NOT include any outstanding loans which you may have, so you can see that you probably would not buy a $364,000 house.

Now, just for fun, let’s use the second calculator that is fixed on your monthly budget - same link, just lower on the page. We know at $90,000 per year annual gross income is $7,500 per month gross income and we want to spend no more than 30% of that so drop $2,250 in the box. We know that we’ll have a 30-year mortgage and the rate is about 6%. Let’s say that our rich uncle is not going to spring for 20% and maybe we can get a loan or grant for some of that downpayment. We’ll change the value from % to $ and drop in $25,000. We’ll keep the tax and insurance rate the same (.65 and .5) and keep the maintenance the same too. Hit calculate and this is the result:

There you have it—you could afford that cute little house! Now, the next piece of the puzzle: what’s your credit score?

We’ll dive into that in the next installment of our Homebuyer Blog Series. Keep following along so you’ll be ready to make that house yours!